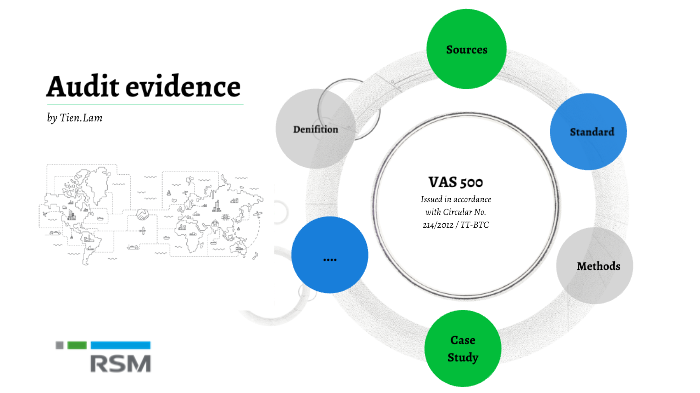

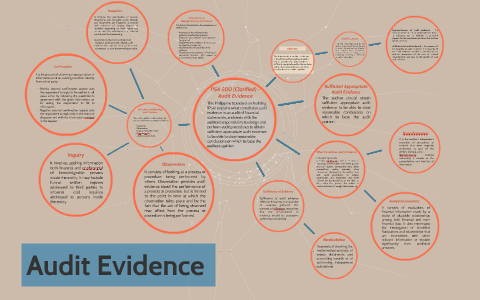

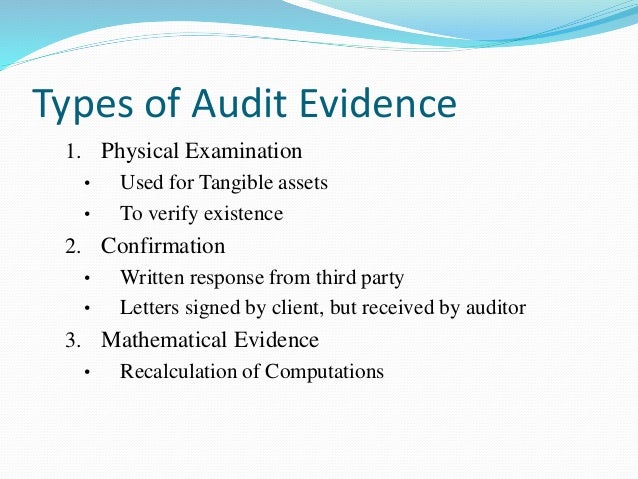

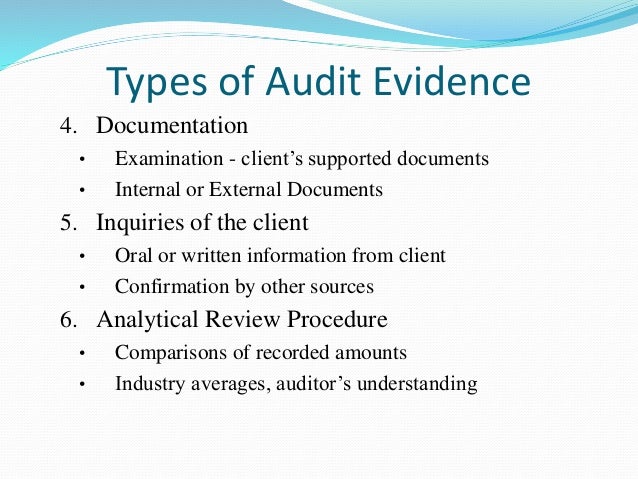

Audit Evidence

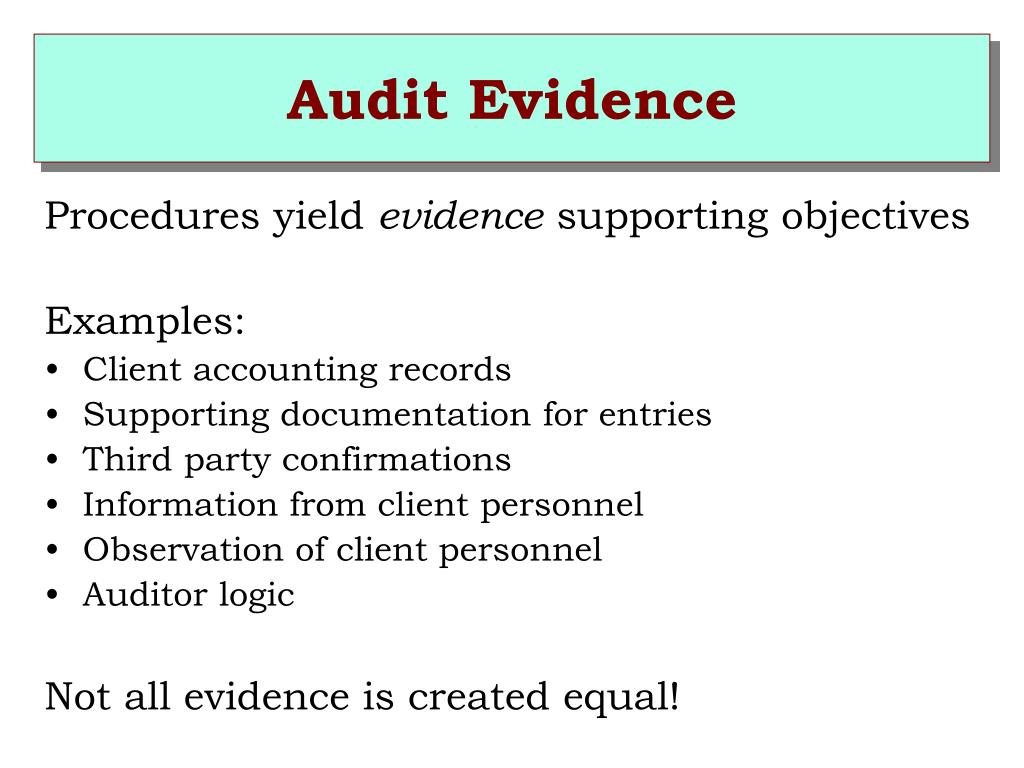

Audit evidence is the information that the auditor uses in arriving at a conclusion on the basis of which he forms his opinion.

Audit evidence. The quality of audit evidence is dependent mainly on the form and source of the evidence. The public company accounting oversight board pcaob created by the. Quality of audit evidence. It is part of auditing work for reviewing and verifying the companys different financial transactions internal control in place and other requirements to express his opinion on the real and fair view of the financial statements of the company during the period under.

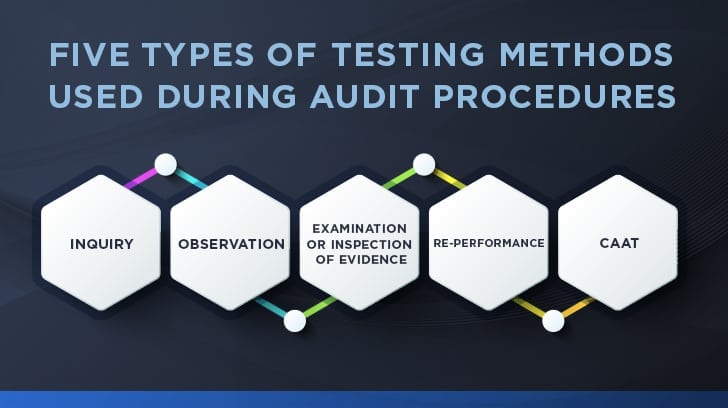

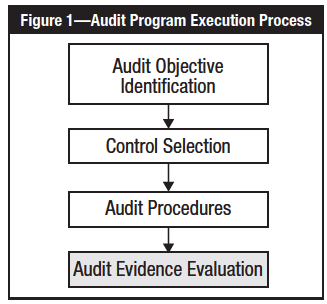

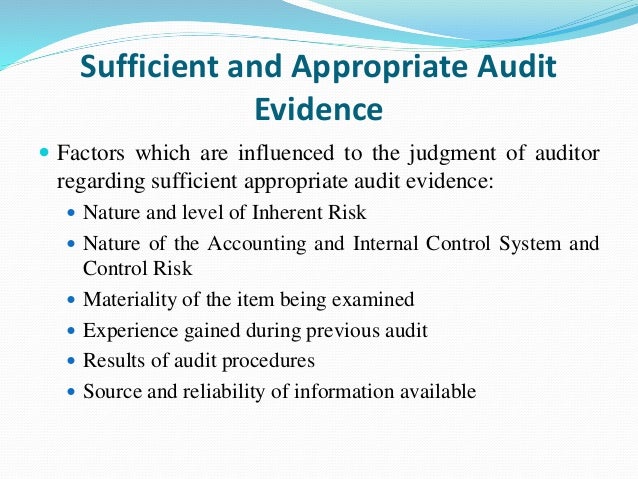

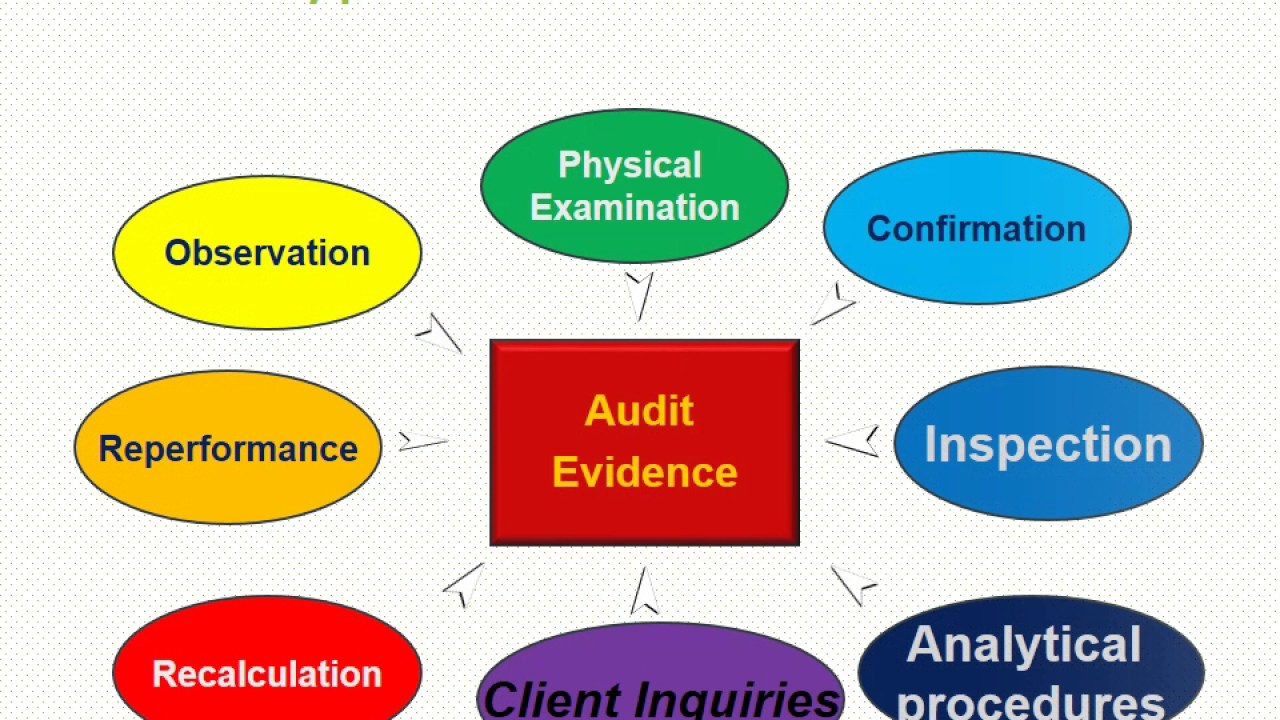

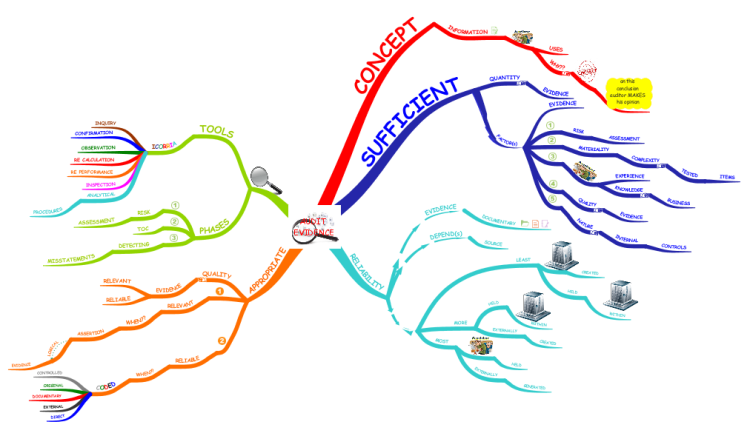

An auditor applies various audit procedure to obtain audit evidence which enables him to form an opinion whether the financial statements of an entity are free from material misstatement and state a true and fair view or not. The quality of audit evidence is very important to make sure that the conclusion that makes by the auditor is correct. It helps the auditor in perceiving the types of evidences available in an audit situation collecting them through the various audit techniques and evaluating their sufficiency and appropriateness to support the accounting data. All audit techniques and procedures are derived from the concept of evidence.

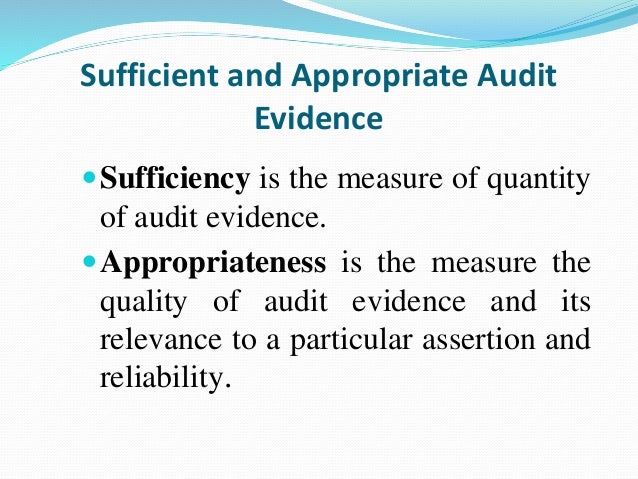

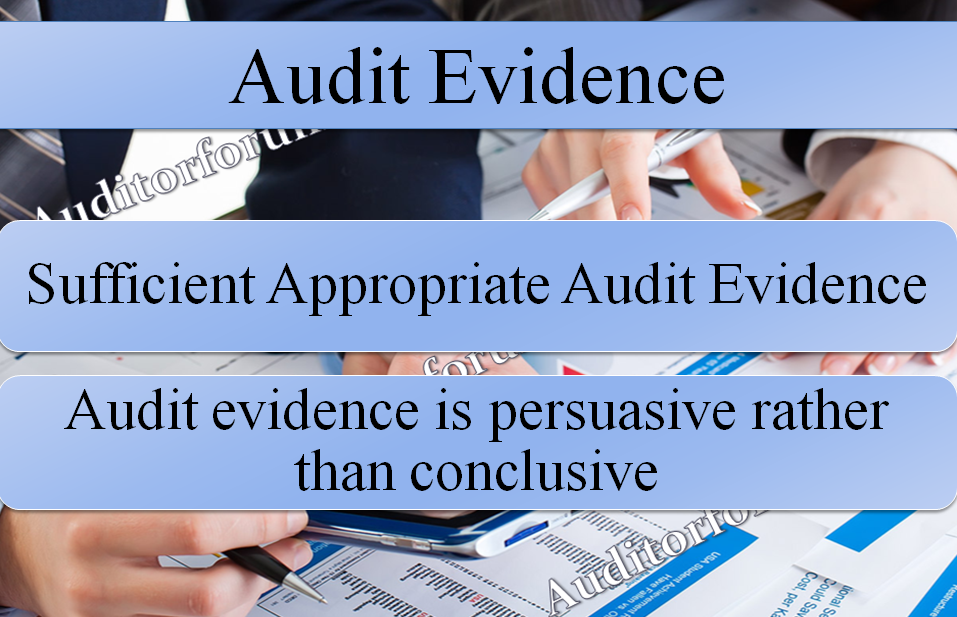

If the information is not strong or low quality the audit risks of making incorrect audit opinions are high. The auditor must plan and perform audit procedures to obtain sufficient appropriate audit evidence to provide a reasonable basis for his or her opinion. Sufficiency is the measure of the quantity of audit evidence. Audit evidence is a reflection of the realities found during the course of an audit.

The audit evidence is the information that the auditor of the company collects from the company.

Audit Working Papers Audit Procure To Pay Financial Statement

Pdca Of Audit Evidence The Auditor

Don T Forget To Ask For Evidence That Audit Guy

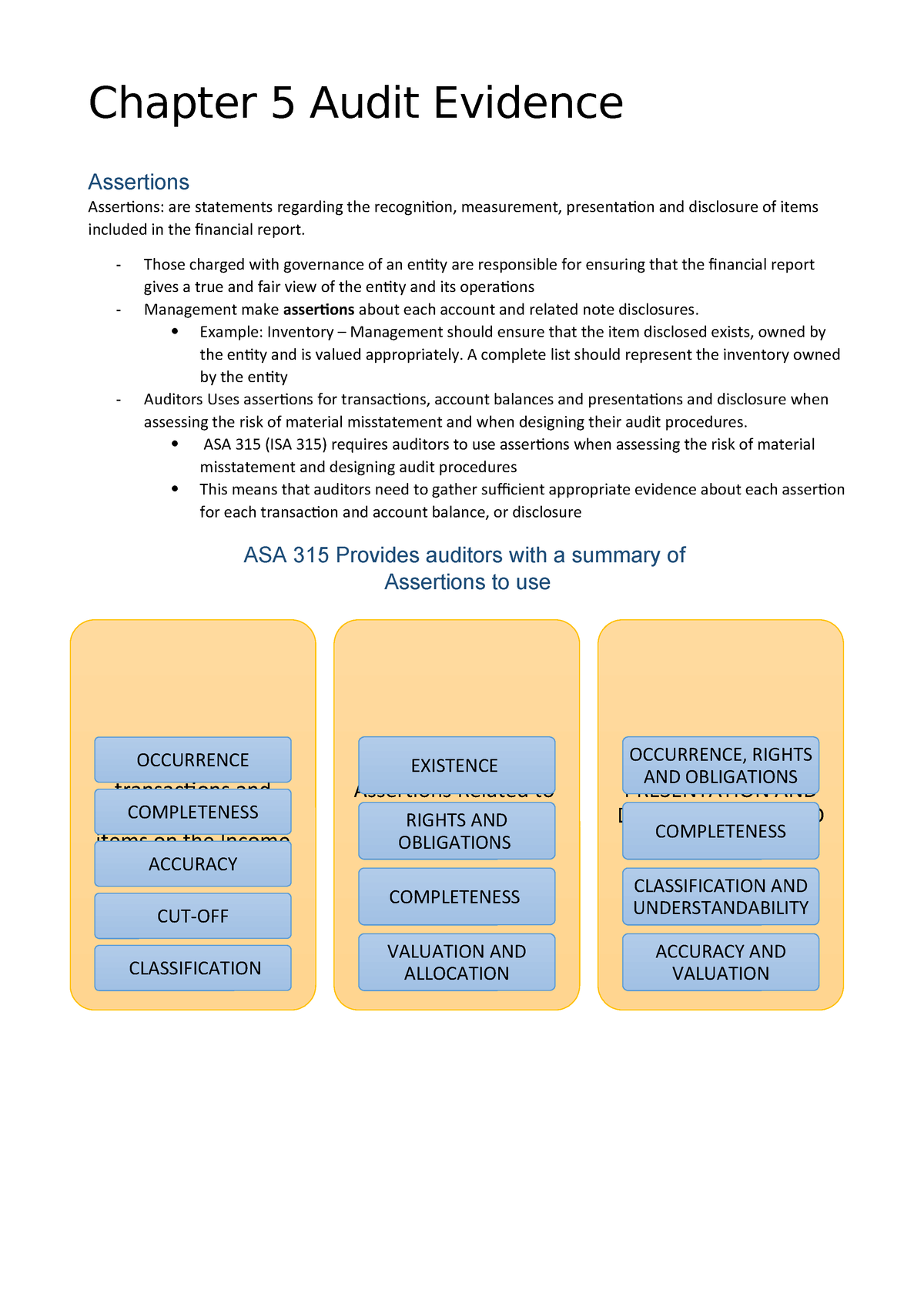

Https S3 Studentvip Com Au Notes 11944 Sample Pdf

Auditing And Accounting During And After The Covid 19 Crisis The Cpa Journal