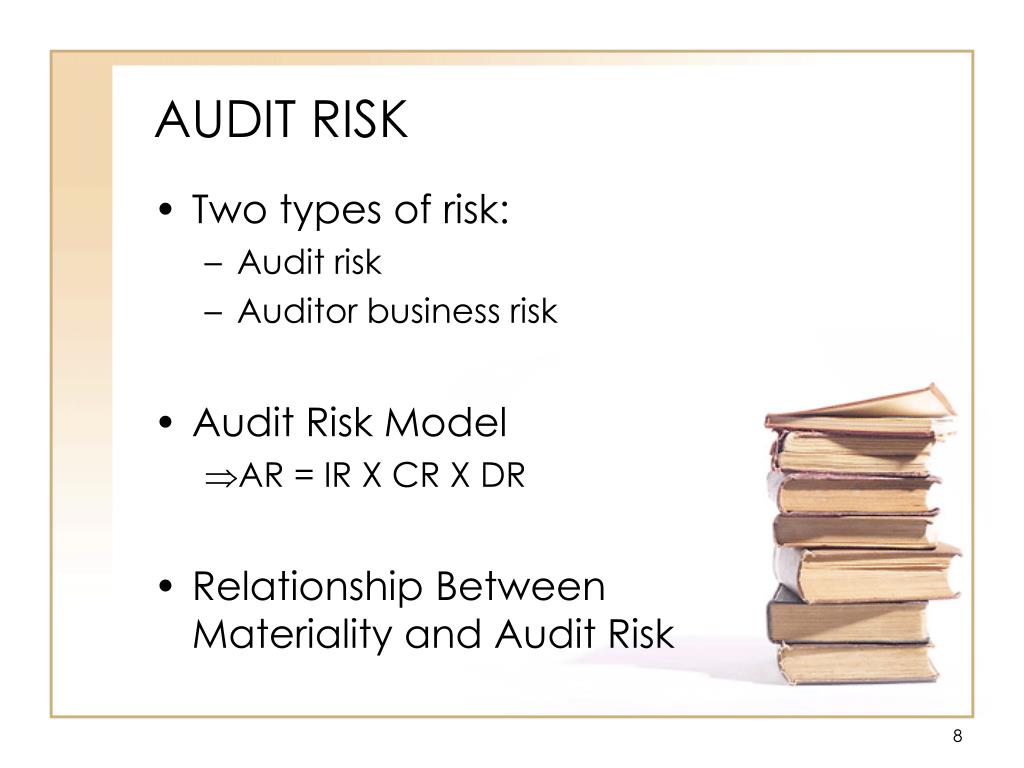

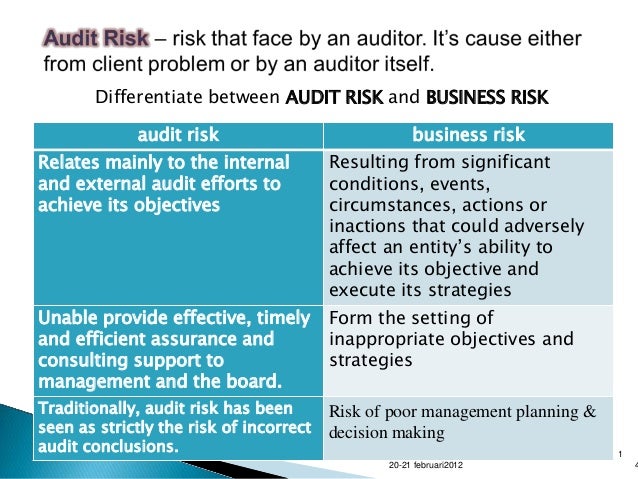

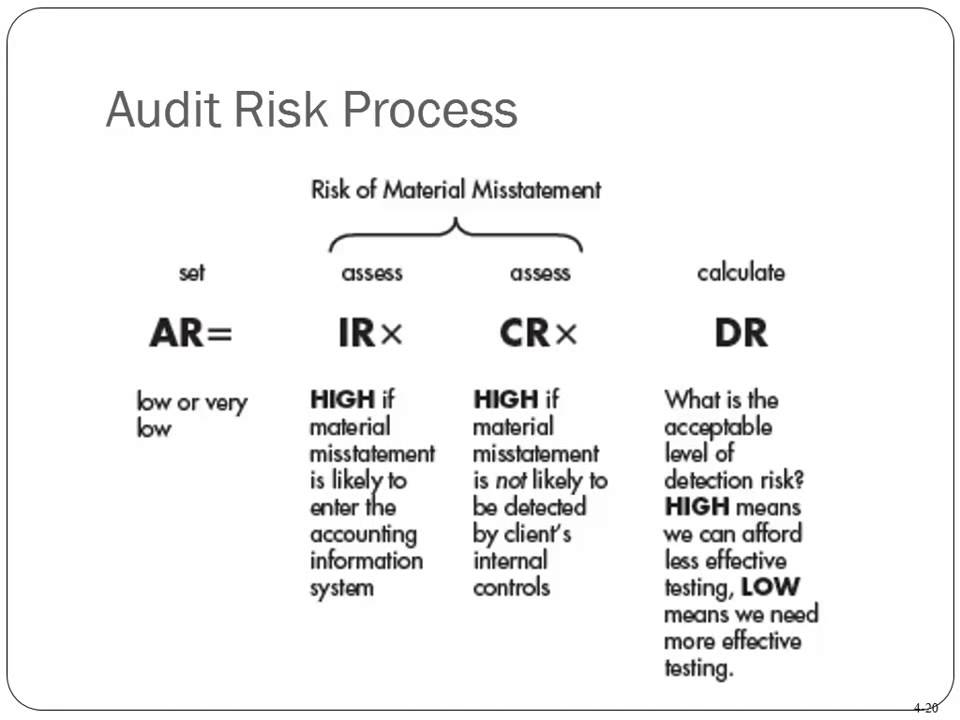

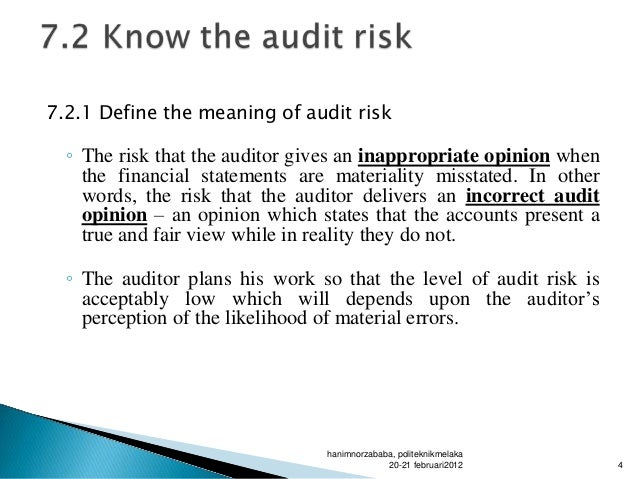

Audit Risk And Materiality Relationship

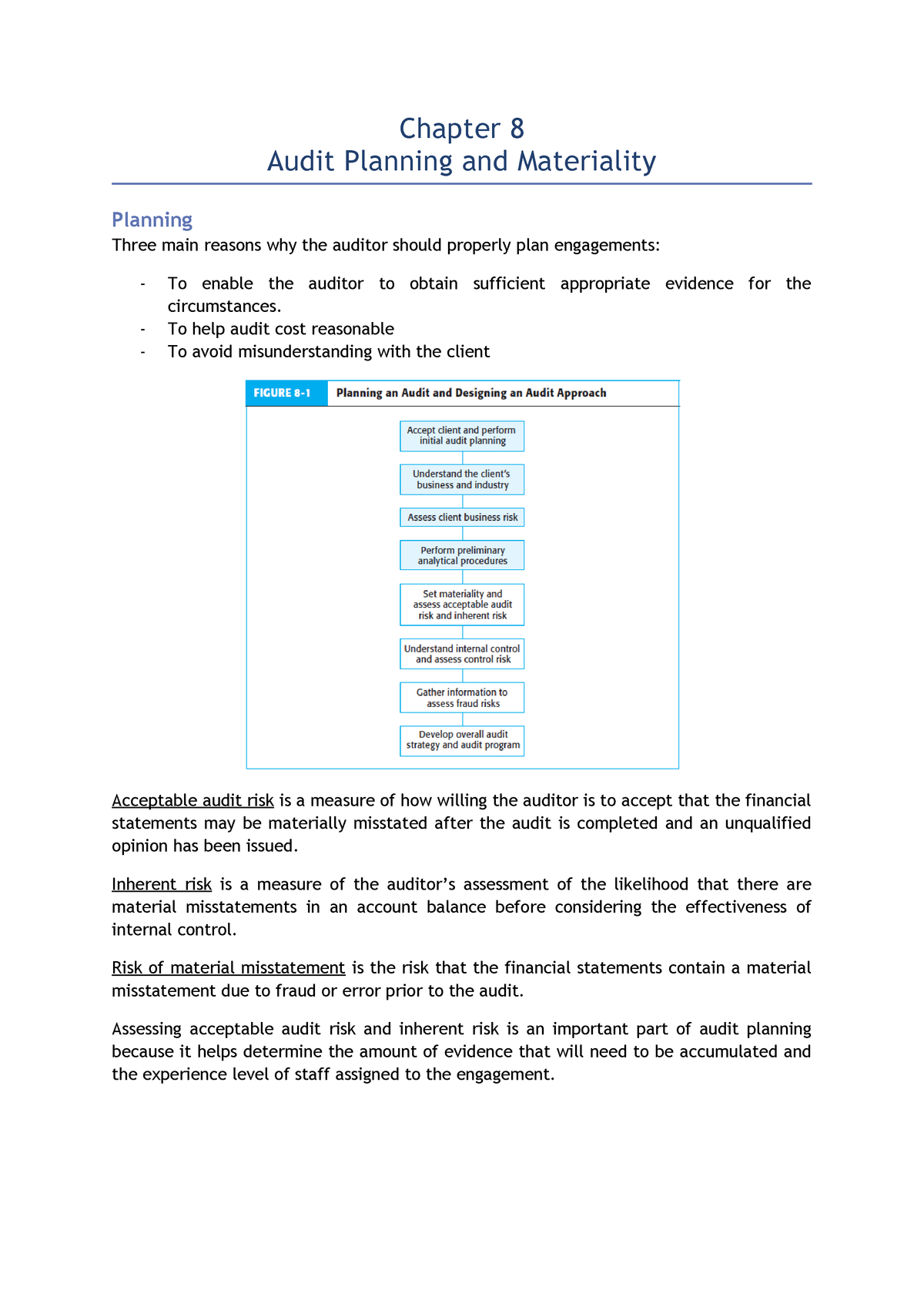

In planning the audit the auditor should use his or her judgment as to the appropriately low level of audit risk and his or her preliminary judgment about materiality levels in a manner that can be expected to provide within the inherent limitations of the auditing process sufficient evidential matter to obtain reasonable assurance about whether the financial statements are free of material misstatement.

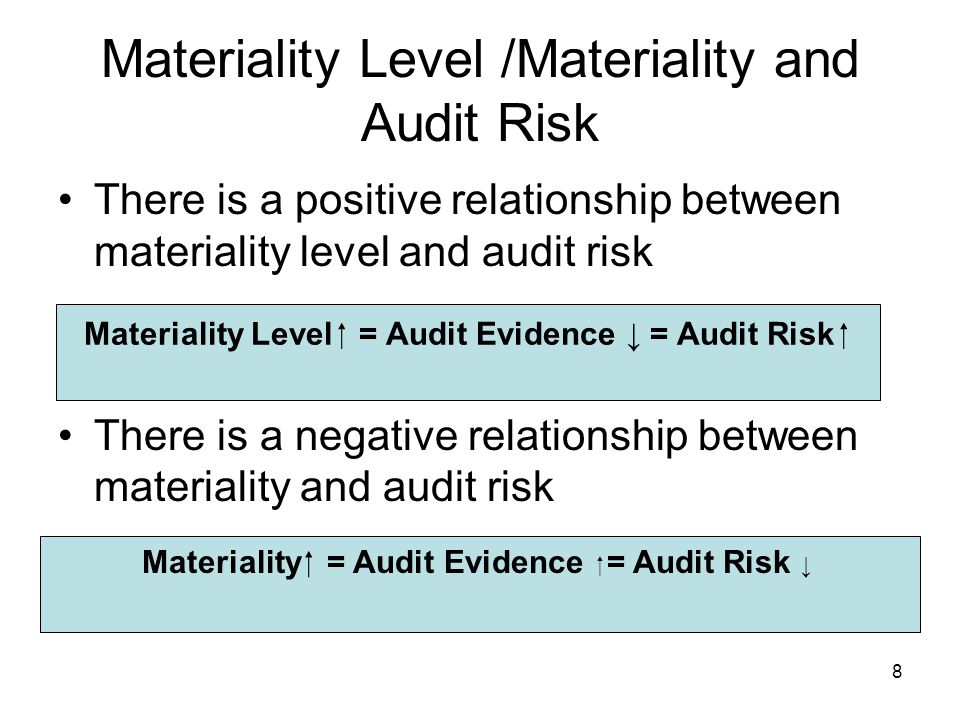

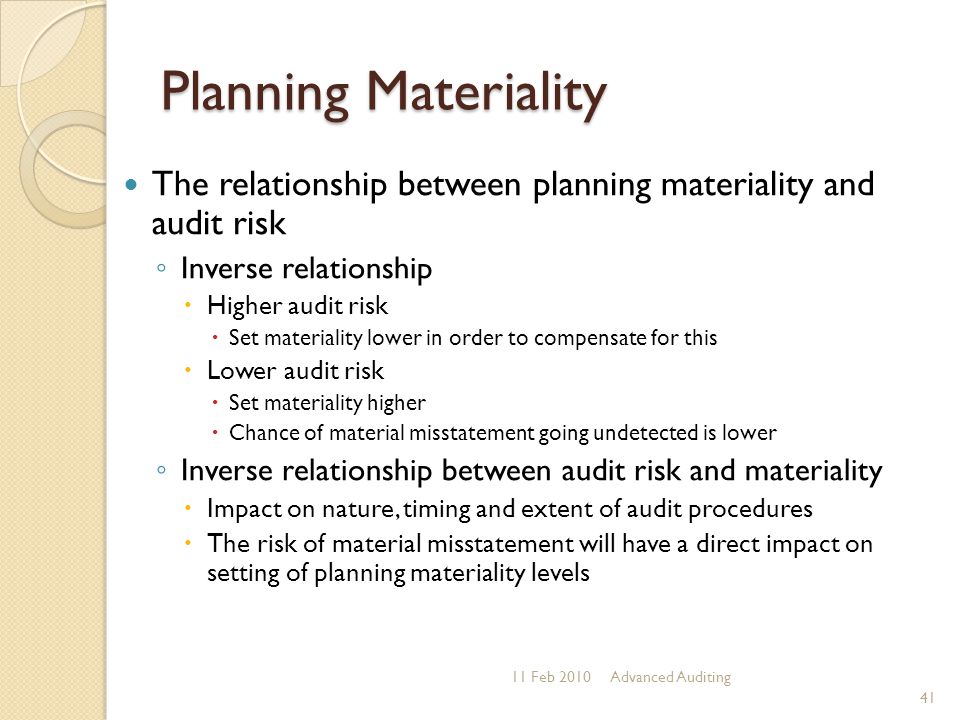

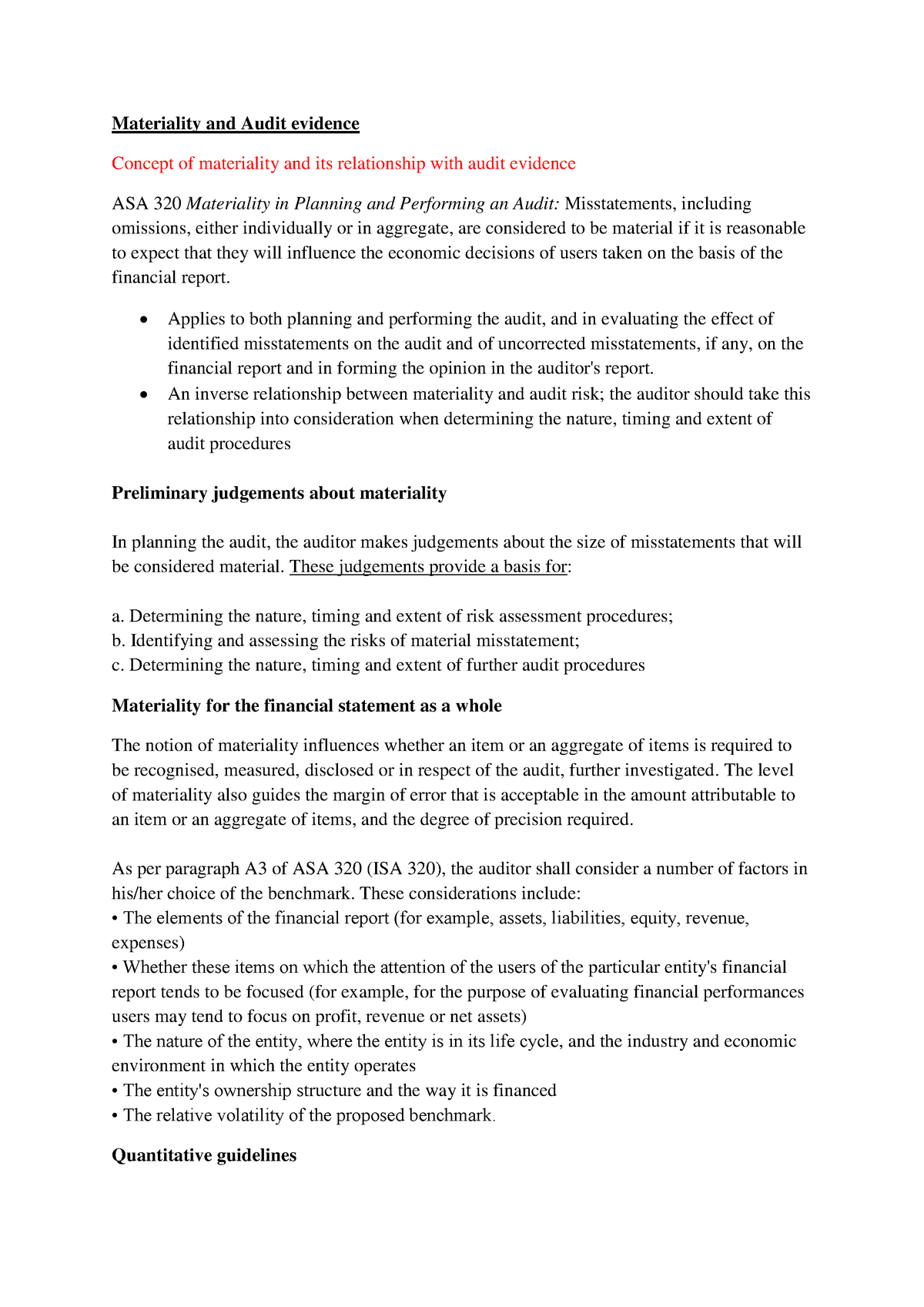

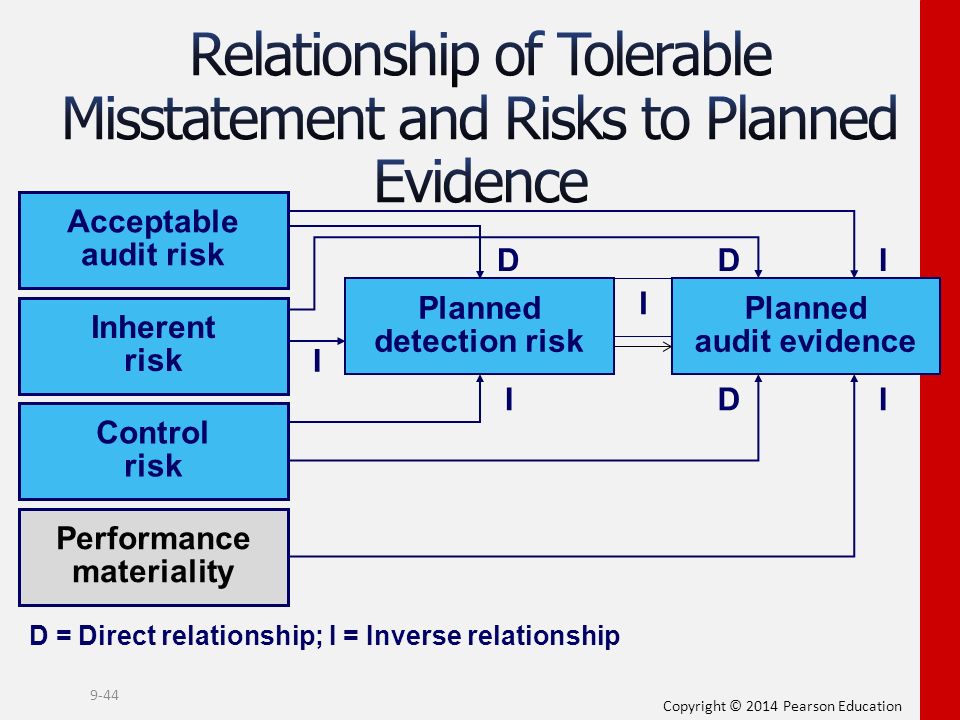

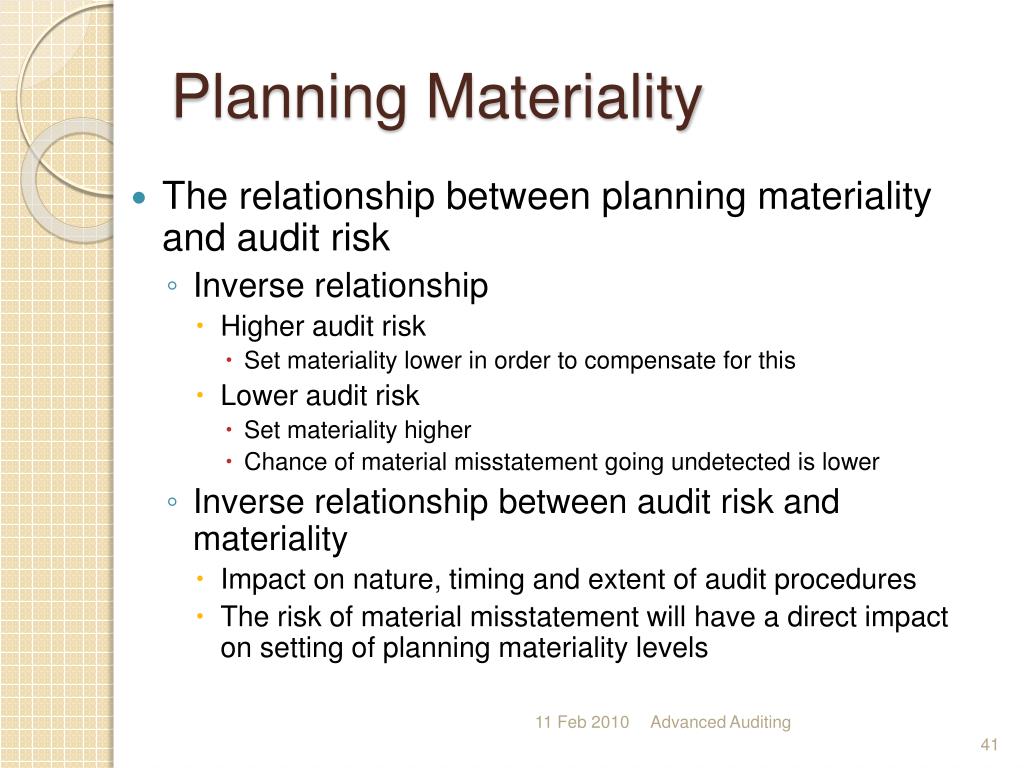

Audit risk and materiality relationship. There is an inverse relationship between materiality and the level of audit risk that is the higher the materiality level the lower the audit risk and vice versa. Such risks may be especially relevant to the auditors consideration of the risks of material misstatement arising from fraud for example through management override of internal control. Auditors take into account the inverse relationship between materiality and audit risk when determining the nature timing and extent of audit procedures. Audit risk and materiality in conducting an audit 1651 the class of transactions account balance or disclosure level.

The auditor takes the inverse relationship between materiality and audit risk into account when determining the nature timing and extent of audit procedures. There is an inverse relationship between materiality and the level of audit risk that is the higher the materiality level the lower the audit risk and vice versa. 5 to 10 of net income. 1 to 2 of gross profit.

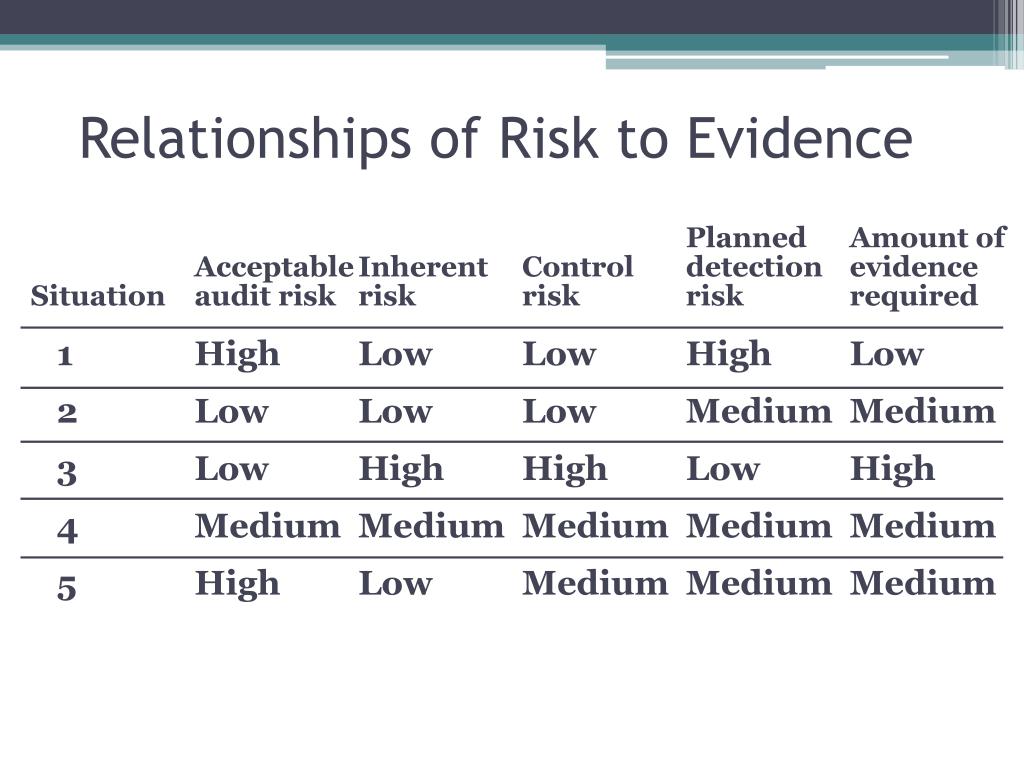

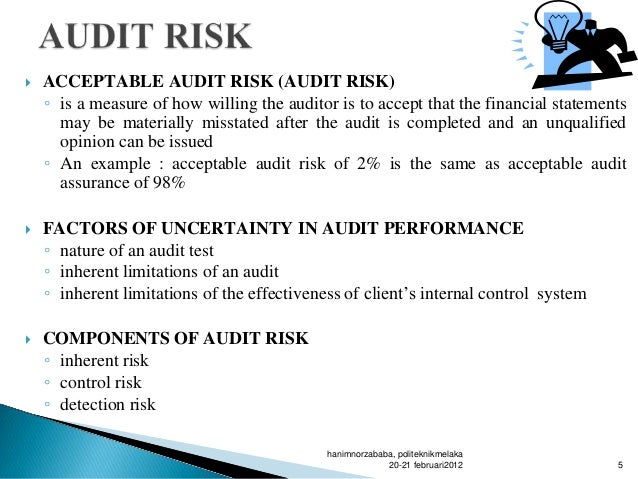

Materiality the threshold for something being significant to the financial statements would be important to users of the fs audit risk the risk that there is an error materiality level that is not detected by the audit team. There is an inverse relationship between materiality and the degree of audit risk. After the auditor has assessed the inherent and control risks he should consider the level of detection risk that he is prepared to accept and based upon his judgment select appropriate substantive audit procedures. Depending on the audit risk auditors will select different values inside these ranges.

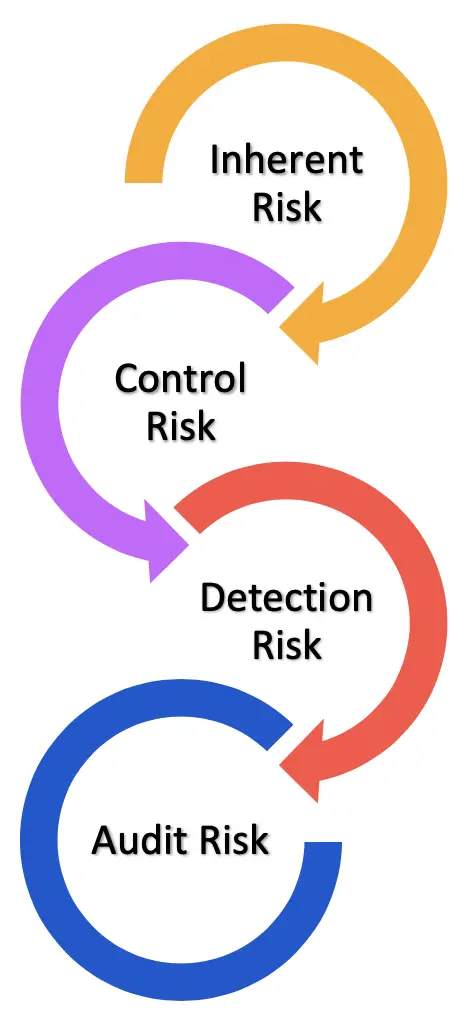

Audit risk may be considered as the product of the various risks which may be encountered in the performance of the audit. Higher the materiality level the lower the audit risk and vice versa. 1 to 2 of total assets. 2 to 5 of shareholders equity.

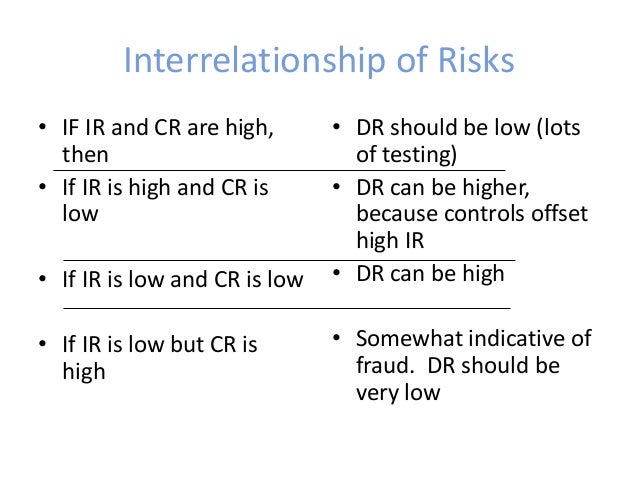

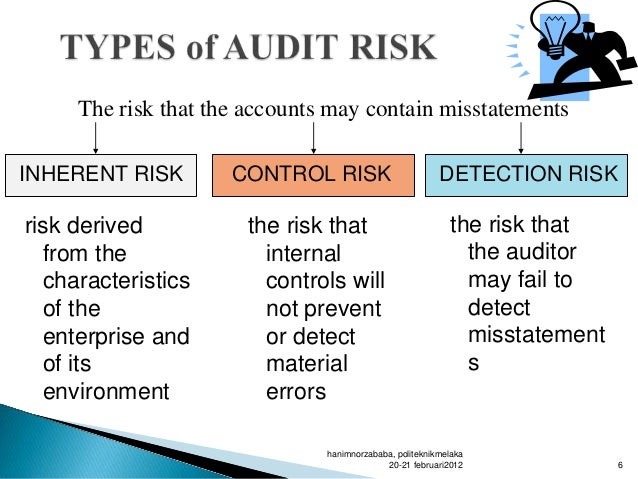

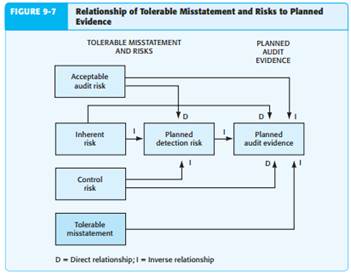

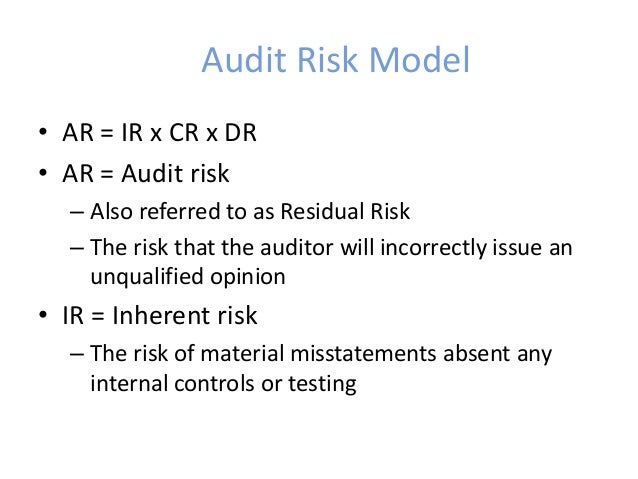

5 to 10 of total revenue. The above figure illustrates these relationships as well as the interrelationship among all three concepts. Audit risk inherent risk x control risk x detection risk. There is an inverse relationship between materiality and audit evidence and an inverse relationship between audit risk and audit evidence.

Materiality In The Context Of Audit The Real Expectations Gap Emerald Insight

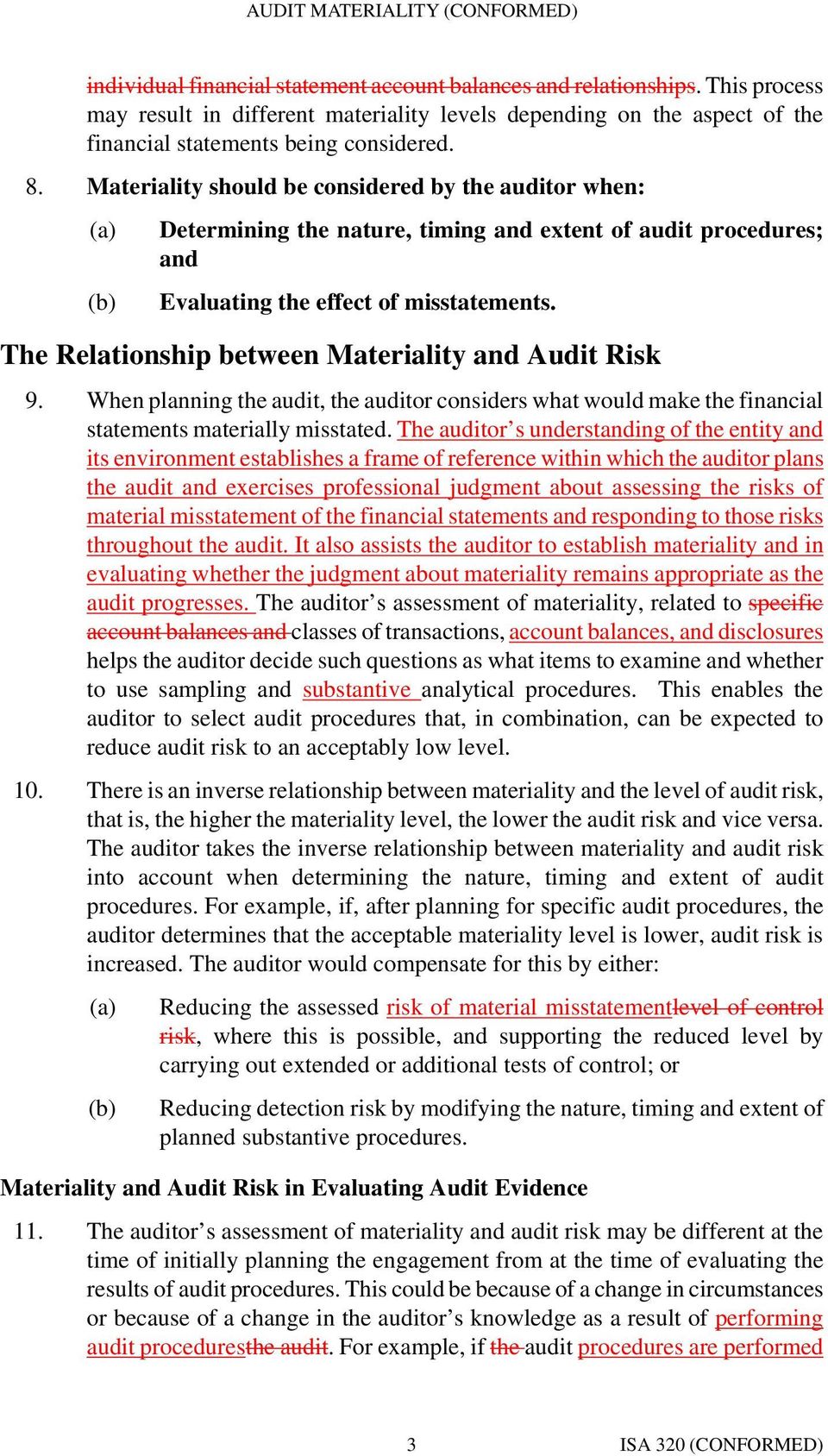

2

Interrelationship Among Materiality Audit Risk And Audit Evidence

Materiality And Risk Youtube

Materiality And Risk Assessment